BEWARE Military Disability Scam

My husband retired from the military in April 2022. It was an awesome occasion when it finally got here; however, getting there was slightly painful. He had to go through tons of briefings on his own. We also had to go through a finance briefing. Because I am who I am, I requested to visit finance several months prior. Nothing irks me more than being made to make financial decisions, before you’ve had a chance to digest the information. I’ll get off that soapbox, because that’s not what today’s post is about.

When a Servicemember Retires

When a servicemember retires, they can receive retirement income, as well as disability benefits. In the process of retiring, servicemembers have to go through a process to determine their disability rating, which can range from 0 - 100% disabled. Just for clarity, that disability rating does not mean there is necessarily a visible physical impairment.

The disability rating will determine if there is any portion of the retirement income that is not taxable. The service members receive two separate payments - retirement income (taxable), and disability income (non-taxable).

The Strickland Rule

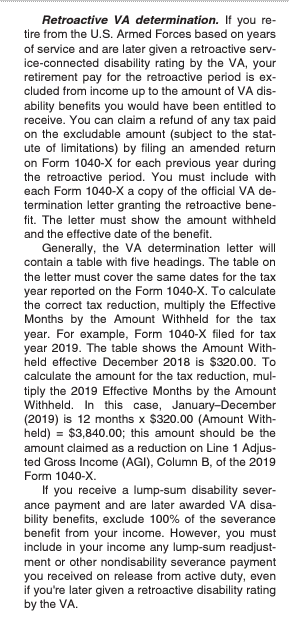

In current times, most service members receive their disability rating at the time they retire, so the payments are accurate. There are situations though, where a service member retires, and then receives a disability rating later on. If that disability rating is made retroactive, then the service member may be entitled to a refund of a portion of the taxes paid.

In Revenue Ruling 78-161, Zebulon Strickland, COL(RET) received a retroactive disability rating. In short, he argued, and it was held, that he was entitled to a refund of taxes paid on the retirement income previously paid during the retroactive time.

The scam that followed…

Your retirement income is not taxable

When my husband retired, a few of his friends sent him an email. It was the exact same email that was sent from different people saying that his retirement income is not taxable, because of his disability rating. Naturally, he sent the email to me.

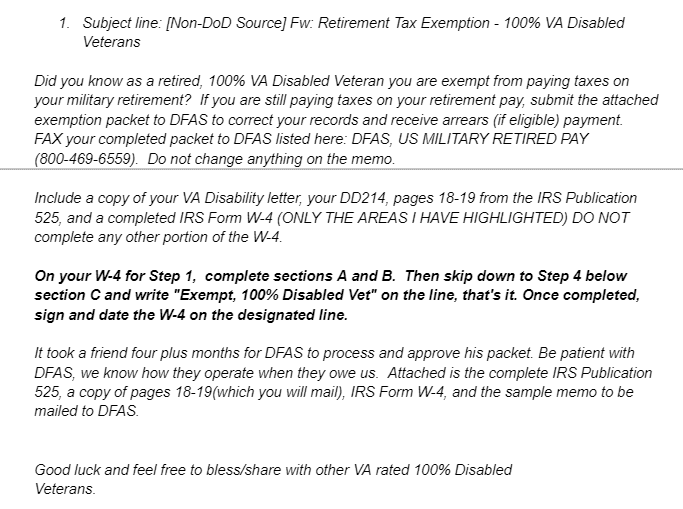

- The attached memo says:

Dear DFAS,

In accordance with the attached IRS Publication 525, because I am 100% disabled, certain

Military and government disability pensions are not taxable. I am requesting to have the code

changed in DFAS to reflect me not paying taxes on my retirement pay.

Thanks for your prompt assistance in this matter.

Writing Exempt on the W-4

Let me tackle the easy one first. If you send a W-4 to payroll with ‘Exempt’ written on it, they will stop withholding federal taxes. That doesn’t mean you won’t owe taxes. It just means you instructed the payroll department to not withhold taxes. When you file your return, your 1099R will show both the distribution amount and the taxable amount, which will be the same. You will have tax liability when you file.

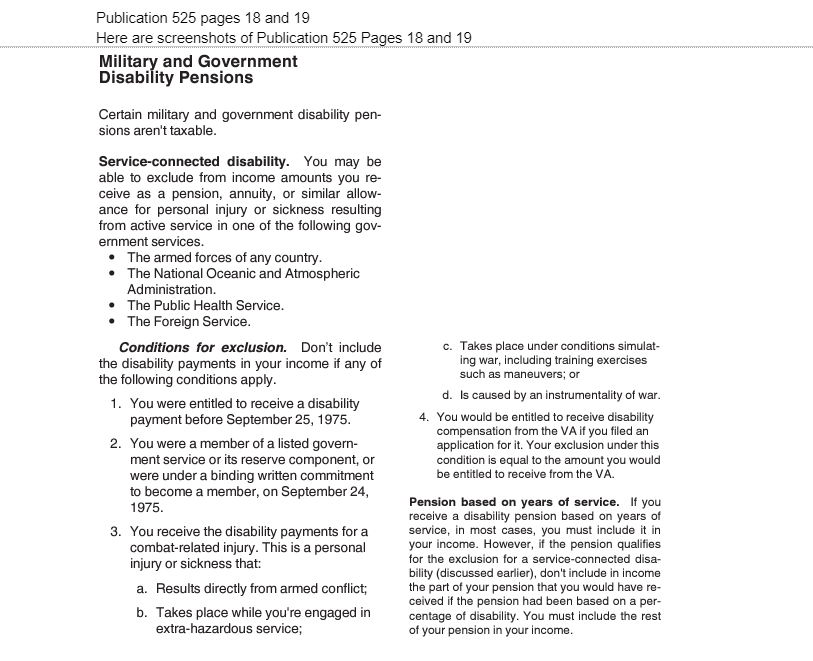

Publication 525

As you can see, Publication 525 does state that certain military and government disability pensions aren't taxable (VA disability), and it lists the terms and conditions. However, it goes on to say that if you receive a disability pension based on years of service (retirement income), in most cases, you must include it in your income (taxable). If the pension qualifies for the exclusion for a service-connected disability, don't include in income the part of your pension that you would have received if the pension had been based on a percentage of disability.

If you get your disability rating at the time you retire, barring any other administrative errors, your retirement pay and disability payments are accurate.

What the packet is attempting to convince you is that your retirement (pension based on years of service) is not taxable, and that is factually incorrect.

For people that actually attempted to amend previous returns to get taxes refunded, here’s what happened. Initially, the servicemember received a refund of the taxes. On audit (a year or 2 later) the government came back for their money, plus interest and penalties. There were several tax preparers pushing this scam, and were eventually barred from the tax preparation industry, and some incarcerated.

Here’s the bottom line:

Tax professionals, if a retired service member says they want to amend to get their taxes back, ask to see their VA Disability rating letter.

If you have back tax debt click here to contact us! We are here to help!

1099K Reporting 2024

There has been another delay in the change of the 1099K reporting. It has also caused more confusion for payors to know if they should issue a 1099K or a 1099-NEC to a provider. Let’s chat about how we got here.

Backstory on 1099K Reporting Change

In December 2020, the Treasury Inspector General of Tax Administration (TIGTA) released the results of a study and found that a lot of taxpayers, who did not meet the 1099K threshold, were not reporting their income. You can read more about the study here.

1099K Requirements

Prior to 2022, the requirements for a third party payment settlement entity (PSE) to file a 1099K were if a payee exceeded $20,000 AND 200 transactions ~ § 1.6050W-1(c)(4)(i)(ii). PayPal, Stripe, Amazon, or EBay are examples of PSEs. Here are a few examples of 1099K reporting.

Example 1: Business owner A used Stripe for payment processing. A earned $150,000 but only had 10 transactions. Stripe was not required to issue a 1099K.

Example 2: Business owner B sold on EBay. B had 250 transactions, but only earned $15,000. EBay was not required to issue a 1099K.

Example 3: Business owner C provided a service and used QuickBooks for invoicing. C earned $25,000 and had 201 transactions. QuickBooks was required to issue a 1099K.

Regardless of whether a taxpayer meets the threshold for 3rd parting reporting, the taxpayer is still required to report the income. All income is taxable unless it is specifically exempted by law. ~§61

Taxpayers became more savvy, and actively avoided 1099K reporting by using different PSEs to stay below the reporting threshold. The legal term for that is structuring, which is illegal.

To combat underreporting income, the IRS proposed lowering the reporting threshold to $600 to match the 1099-NEC threshold. PSEs (and the public) lost their minds. Suddenly it was viewed that the government was now coming to tax income that wasn’t previously taxed. That was NEVER the case. Taxpayers were not reporting their income as required.

States 1099K Reporting Requirements

Even though Federal Laws have not changed, some states have reduced their 1099K filing requirements. Washington DC, Virginia, Maryland, are a few states that have a $600 threshold for 1099K filing. You can review a complete list of state 1099K requirements here. That means if you live in one of the states with reduced requirements, you'll receive a 1099K, even though it's less than the Federal requirement.

1099K vs 1099-NEC

As the discussion raged about the 1099K, so did confusion about whether one should issue a 1099-NEC to service/product providers or if the 1099K would suffice. A 1099K covers digital payments like credit cards, debit cards, or on third party platforms like the ones listed above. A 1099-NEC is used for payments through cash, ACH, or paper checks.

Example: Let’s assume you pay a landscaper $650 by check, you may be required to issue a 1099-NEC. Note: 1099-NECs are not issued to corporations.

Let’s assume in the same example you paid the landscaper $650 by credit card. The payment processor is required to issue the 1099K when the user reaches 1099K thresholds. You would not be required to issue a 1099-NEC.

When people are confused about the law, they issue the 1099-NEC to be on the safe side. While that may seem like the best thing to do, it really isn’t. You create an issue of double-reporting when you issue a 1099-NEC that is not necessary.

The IRS looks at the amounts reported on 1099Ks and 1099-NECs and adds them up. If the reported gross income is less than the 3rd party amounts reported, the taxpayer will receive a notice of underreported income (CP2000).

Example: You paid a contractor $20,000 via credit card, and issued a 1099-NEC. The payment processor also issued a 1099K for $160,000 (that includes the $20,000 you paid by credit card). In the IRS’s view, the contractor earned $180,000, when in reality only $160,000 was earned.

If you have questions concerning the 1099K, check out the IRS updated 1099K FAQ.

If you have an issue with unreported income, click here to schedule an appointment with us!

Employee Gifts are Taxable

I was perusing the news a few weeks ago. The news headlines said, “Wal-Mart Slammed After Gifting Employees 55-Cent Ramen Noodles” for working during a blizzard. Needless to say, Wal-Mart was dragged on Social Media. While I agree, it’s a cheap “gift”, it also made me think of other headlines of similar disdain, like this one: A bus driver retired after 50 years, and ‘all’ they gave him was replica of a bus with his picture on it.

Did you know that most employee gifts are taxable?

De minimis Gifts are not taxable

A De minimis gift is a non-cash gift or award, considering its value and the frequency with which it is provided, is so small as to make accounting for it unreasonable or impractical. In the Wal-Mart example, 55-cent Ramen Noodles would definitely qualify as de minimis. It was a one-time inexpensive gift.

Internal Revenue Code 132(a)(4) excludes de minimis gifts from income (meaning not taxable to the receiver).

Examples of De minimis items not included in taxable income

- Controlled, occasional employee use of photocopier

- Occasional snacks, coffee, doughnuts, etc.

- Occasional tickets for entertainment events

- Holiday gifts

- Occasional meal money or transportation expense for working overtime

- Group-term life insurance for employee spouse or dependent with face value not more than $2,000

- Flowers, fruit, books, etc., provided under special circumstances

- Personal use of a cell phone provided by an employer primarily for business purpose

Cash gifts are taxable

Cash is considered wages, unless an exception applies. An example would be OCCASIONAL meals or transportation. If the meals or transportation becomes a regular occurrence, it will become taxable as wages.

Cash or cash equivalents, such as gift cards, are always taxable income. Gift cards/certificates for general merchandise are never excluded from taxable income. If Wal-Mart had given each employee a Wal-Mart Gift Card for 55 Cents instead of the Ramen Noodles, the 55 cents would have been added to their taxable income.

Achievement Awards can be taxable

Let’s look at the example of the bus received after 50 years of service. Working as a faithful employee for 50 years is DEFINITELY an achievement. Nothing could ever show someone how much they appreciate 50 years of service, but a dinky bus?

Internal Revenue Code 274(j) limits the deduction allowed for achievement awards equal to that of the max exclusion amount. The deduction is limited to $400 or $1600 depending on whether it is a qualified or non-qualified plan award, which means that the receiver can only exclude $400 or $1,600. If the value of the achievement award exceeds one of these two numbers, the overage would be taxable.

Internal Revenue Code 274(j)(3) states that achievement awards are tangible personal property awards and:

- Cannot be disguised wages

- Must be awarded as part of a meaningful presentation

- Cannot be cash, cash equivalent, vacation, meals, lodging, theater or sports tickets, or securities.

Imagine getting a vacation with a side of a tax bill

The achievement awards can't be any of the cool things one would like to receive as an achievement award. When all of social media is screaming that an employer should send the 50-year employee on a trip, instead of giving the employee the stupid bus, tax law says... NO!

Let’s assume the total value of that trip is $8,000. The final W-2 would include an $8,000 increase in income for which the employee paid no taxes. Can’t you just see it? “Congratulations on 50 years! Here’s a 2 week all-inclusive vacation to Jamaica for you and your family.”

The additional income would increase the tax liability or reduce a refund. It’s not like the employee received $8,000 in cash, so s/he could reserve cash funds. How NOT awesome would that be?

Can companies ‘afford’ to give employees ‘better’ gifts? Unequivocally yes! However, tax law says they can’t, unless the employee pays taxes on the value of the gift. Wal-Mart gave employees a pack of noodles worth 55 cents. One would think they could have at least sprung for two.

If back taxes or unpaid tax debt are keeping you up at night, click here to reach out to us! We’re here to help!

Can Service Providers Issue a 1099-C for Unpaid Bills?

Social media never fails to provide the most false or misleading tax information. This post did not disappoint. The social media post said:

$130K in unpaid contracts over here.

I don’t argue. I have forgiven their debt on my end with a 1099-C.

Now it’s between them and the IRS beloveds. It’s above me now.

If you do B2B transactions do not argue. Make their debt to you taxable. They do not get to claim a tax break when they did not start or finish paying you.

Protect your business and your blood pressure 😊

The post was made by a service provider who had unpaid bills. The post had 20 comments and 597 likes. Almost 600 people saw this post, and thought 'this is really cool'. A few others commented that 'this was an education', and others stated that they were going to do this ASAP! Uhhh NO!!

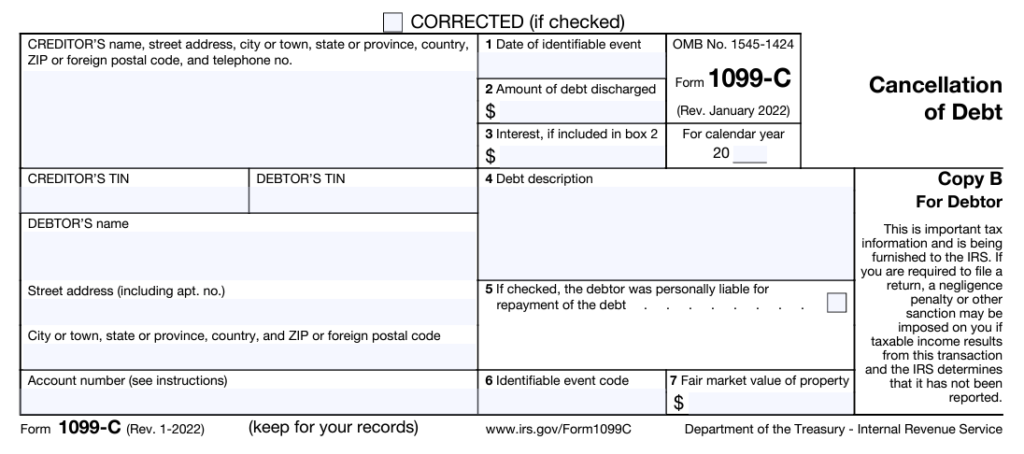

Purpose of a 1099-C Cancellation of Debt

The IRS form 1099-C, Cancellation of Debt, is designed for financial institutions (such as banks) to report a cancellation of debt [usually related to non-payment] of $600 or more. This cancellation of debt, most often, is treated as taxable income to the debtor, and must be claimed on the tax return. A creditor/debtor relationship is established. There is a loan amount, loan payment terms, interest rate, and methods of resolution in the event of default (non-payment).

Who Can File a 1099-C

Internal Revenue Code 6050P makes a specific list of entities who can file a 1099-C:

- A financial institution described in section 581 or 591(a) (such as a domestic bank, trust company, building and loan association, or savings and loan association).

- A credit union.

- Any of the following, its successor, or subunit of one of the following.

- Federal Deposit Insurance Corporation.

- National Credit Union Administration.

- Any other federal executive agency, including government corporations.

- Any military department.

- U.S. Postal Service.

- Postal Rate Commission.

- A corporation that is a subsidiary of a financial institution or credit union, but only if, because of your affiliation, you are subject to supervision and examination by a federal or state regulatory agency.

- A federal government agency including:

- A department,

- An agency,

- A court or court administrative office, or

- An instrumentality in the judicial or legislative branch of the government.

- Any organization whose significant trade or business is the lending of money, such as a finance company or credit card company (whether or not affiliated with a financial institution). The lending of money is a significant trade or business if money is lent on a regular and continuing basis.

Please note that you do not see a service provider with an unpaid bill in the list.

Providing a Service does not create a Creditor/Debtor Relationship

When a service provider engages a client for services, It creates a provider/client relationship. A service provider agrees to perform a service in exchange for an agreed amount. There are remittance (payment terms), such as payment due in 15 days, due immediately upon completion, or due in advance. While this is a contract, it does not create a creditor/debtor relationship. The service provider is not lending money to the client.

Filing a False 1099-C Consequences

This service provider seemed really snappy and clappy, seemingly to believe that she will cause their client to have an unexpected tax bill. However, should she issue a 1099-C for an unpaid bill, there are consequences.

Internal Revenue Code 7434 states:

If any person willfully files a fraudulent information return with respect to payments purported to be made to any other person, such other person may bring a civil action for damages against the person so filing such return.

https://www.law.cornell.edu/uscode/text/26/7434

The person filing the false 1099-C can be liable for the GREATER of $5,000 or the sum of damages, costs of the action, and attorney's fees. A plaintiff (the one who received said 1099-C) has 6 years from the date the false 1099-C was filed or 1 year after the return would have been discovered with reasonable care. Oh yeah, the IRS wants a copy of the suit, as well.

It can be quite frustrating when you provide a service to your client, and they don't pay the bill. You can go through a collection agency to try to recoup your money. You cannot deduct the amount of unpaid funds, unless you're using the accrual method of accounting. The only reason it is a deduction for the accrual method is that you've already counted the income. Regardless, issuing a 1099-C is not the method for service providers to collect their unpaid funds.

If you are dealing with back taxes or unpaid tax debt, reach out to us! We're here to help!

BENEFICIAL OWNERSHIP INFORMATION REPORTING 2024

Phase 1 of the Corporate Transparency Act (CTA) went into effect on January 1, 2024. It imposes a new federal filing requirement for most corporations and limited liability companies (LLCs) formed in 2024 and later. It also applies to businesses formed before January 1, 2024, but the requirements are different. See the note at the bottom of the post.

What was the Corporate Transparency Act all about?

Usually when the government creates new laws and requirements, it’s in an effort to curtail criminal activity. This is no different. The purpose of CTA is to attempt to prevent anonymous shell companies for money laundering, tax evasion, and other illegal purposes. As with everything else, the good get caught up with the bad, hence BOI Reporting. #ThanksCriminals

The BOI Report applies to businesses formed by filing with the Secretary of State, such as LLCs and Corporations. Some businesses are exempt. You can find the list of exemptions here. If you are unclear as to whether or not you are exempt, file the BOI report. One of my tax mentors told me once, ‘There is no such thing as over-reporting. When in doubt, REPORT!’

Deadline to file BOI Report

Applicable companies that were formed January 1, 2024 or after, have 90 days to file the BOI report. The report is filed at: https://www.fincen.gov/boi. The report contains specific information for each beneficial owner.

According to FINCEN, a beneficial owner is defined as “any individual who, directly or indirectly, exercises substantial control over a reporting company, or who owns or controls at least 25 percent of the ownership interests of a reporting company.”

Here is the information you’ll need for each Beneficial Owner to complete the BOI Report:

- Full legal name

- Date of birth

- Complete current residential street address

- A unique identifying number from a current U.S. passport, state or local ID document, driver’s license, or foreign passport

- An image of the document that contains the unique identifying number

BOI Company Applicant

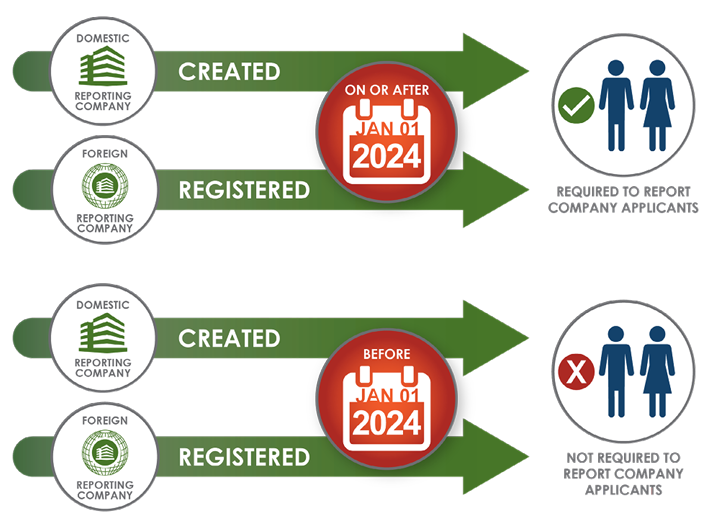

A company applicant is defined as either the "direct filer, or the individual who directs or controls the filing action". A reporting company is also required to report its company applicants if it is either a:

• domestic reporting company created on or after January 1, 2024; or

• foreign reporting company first registered to do business in the United States on or after January 1, 2024.

Each reporting company that is required to report company applicants will have to identify and report to FinCEN at least one company applicant, and at most two. All company applicants must be individuals. Companies or legal entities cannot be company applicants.

Who is responsible for filing the BOI report?

There is a lot of misinformation about who is actually responsible for filing the BOI Report. The responsibility belongs to the Beneficial Owner(s). The BOI Report is NOT a tax report, therefore your tax professional or accountant is not responsible for filing this report. Can they offer the service? Sure. However, it is not a part of tax preparation, just as filing your annual report with the state is not a tax preparation function. Attorneys are also available to assist you with filing the report. If you hire someone to provide this service for you, trust but verify. The ultimate responsibility lies with the Beneficial Owner(s), not the person you hired.

What if you don’t file the BOI Report?

There’s always someone who asks, “What if I don’t want to?” The willful failure to report may result in a civil or criminal penalties, including civil penalties of up to $500 for each day that the violation continues, or criminal penalties including imprisonment for up to two years and/or a fine of up to $10,000. Senior officers of an entity that fails to file a required BOI report may be held accountable for that failure. Responsible persons can also be penalized for providing false or incomplete information to a company, knowing that it is intended to be reported to FINCEN.

To be clear though, nobody is coming to your house to arrest you today for not filing your BOI Report. People are advertising in a way to frighten you to hire them. The earliest anyone has a report due is March 31, 2024.

30 Days to update the BOI Report

Once the initial report is filed, a Beneficial Owner has 30 days to report any changes to Beneficial Ownership. If a Beneficial Owner moves, you must update the BOI report within 30 days. If a company adds an owner, you must update the BOI report within 30 days.

Note: If you formed your business before 1/1/2024, you have until 1/1/2025 to file your report, and you are NOT required to report your company applicant. If your company is created or registered on or after January 1, 2025, it will have 30 calendar days to file its initial BOI report.

BOI Small Entity Compliance Guide

FINCEN created the Small Entity Compliance Guide to answer your questions. Grab a copy here!

The New Self Employed Covid Credit

Ahhh… Have you seen the ads?

“1099 Gig Workers Claim up to $32,000 with the ‘New’ Covid Self Employed Tax Credit (SETC).

Oy! I decided to write this blog post once I got a few inquiries from my clients. Quite frankly, these companies make my skin crawl. I’ve even seen influencers, who have ZERO experience with tax, telling their audiences to go ‘get this money’, BUT ... ‘check with your CPA first’. [Insert my best side-eye.]

The actual name of the credit is the Self-Employed Sick and Family Leave Credit. SETC is not a thing. If you ask a tax professional about the SETC, they’ll probably be confused, because that’s not the name of the credit. However, to gain understanding about this credit, I will use the Street Committee Name - SETC. Let’s talk about how we got here.

Employee Retention Credit Claims - FROZEN

In September 2023, the IRS ordered the immediate stop to Employee Retention Credit (ERC) processing. They received several millions of ERC claims, many of them fraudulent. Employers could still submit claims, but they would not be processed. FYI, Tax Year 2020 ERC claims need to be submitted no later than April 15, 2024. The credit is claimed on Form 7202.

ERC claims were lucrative, and these companies made a BOATLOAD of money, charging 20% of the credit received. If a client received a claim for $60,000, the companies would be paid $12,000. That's a heck of an incentive to submit fraudulent claims. Should the IRS come knocking, it would be at the employers' doors, not the company that fabricated the information on the claim. The IRS pumped all the brakes on that.

SETC is the new ERC

Since the ERC well dried up, these companies shifted their sights to the Self-Employed Sick and Family Leave Credit. Now Self-Employed individuals are being bombarded with advertisements of being able to get ‘up to’ $32,000 from the SETC. It only takes a few minutes to apply (insert affiliate link). You didn't think people were posting about it just to help - right? I'm not mad at anyone earning affiliate commissions. I do it all the time. I AM annoyed at promoting something that has serious consequences if the person doesn't get all the information. A tax credit is not the same as promoting the latest email marketing tool.

Under the 2020 rules, a self-employed individual could claim up to $15,110. For 2021, they could claim up to $17,110; hence the total $32,000. The clock is ticking on claiming the 2020 tax credit, so the ads are on fire.

Qualifications for Self-Employed Tax Credit

There are three main questions you have to answer to determine if you qualify for the credit.

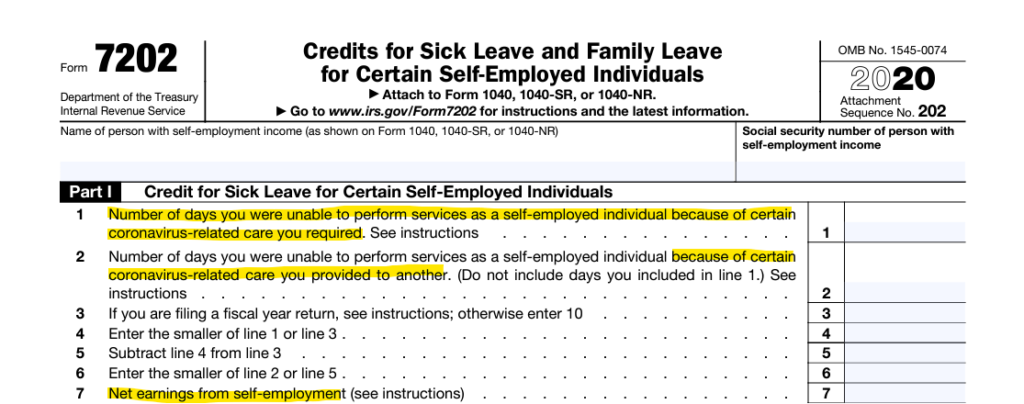

- Were you unable to work because you had Covid?

- Were you unable to work because you had to care for someone with Covid?

- Did you earn a profit?

In 2021, the qualifications were tweaked a bit. In part II of the form below, Form 7202 specifies “January 1- March 31, 2021”, and also specifies caring for a son or daughter (see instructions). The instructions say: “because of certain coronavirus-related care you provided to a son or daughter whose school or place of care is closed or whose childcare provider is unavailable for reasons related to COVID-19 or for any reason you may claim sick leave equivalent credits.

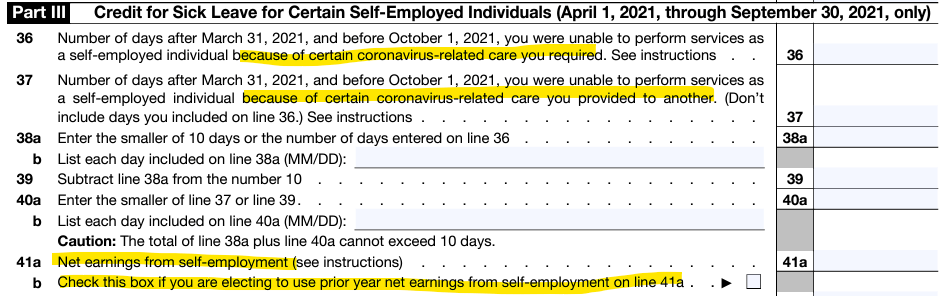

Part III of the 2021 version of Form 7202 specifies April 1 through September 30, 2021, for yourself or care you provided to another. The section specifically for children was removed. The great thing about the credit is that you could separate the time you needed to care for yourself or another from the time you needed to care for your children.

Part III 2021 Form 7202

Plenty of Self-Employed individuals were impacted by Covid. I don’t know any that were not; however, being impacted by Covid did not automatically mean you qualified for the credit. Millions of self-employed individuals lost money in their businesses during Covid. If you look at both the 2020 and 2021 Form 7202, it asks for ‘net earnings’ from self-employment (amount of profit). If you claimed a loss, you did not qualify for the credit. The advantage of the 2021 version of the credit is that you could use net earnings from 2020. If you posted a loss in 2020, then you still did not qualify for the credit.

Be prepared for an audit

If you qualify for the credit and didn’t claim it, by all means, amend your return to claim your credit; however, I also caution you to be ready for an audit. The auditor will ask for bank statements to confirm revenue and expenses. They may also ask for proof that you had Covid, a family member had Covid, or that your childcare facility or school was closed. Closed daycare and schools won’t be hard, for sure. While your health information may be protected, your banking information is not. You have to be able to prove anything you claim on your return.

Don’t be duped into claiming false credits. The false claims are why there is a moratorium on the Employee Retention Credit. If the IRS or State comes knocking on your door (figuratively, they’re not coming to your house right now), but if you get the letter being notified of an audit, reach out to us at ETS Tax Relief to help you!

Kanye West Says He Owes $50 Million in Taxes

Kanye West claims he owes $50,000,000 in taxes. Here we are again, with yet another celebrity that seems to be in tax trouble. I’m side-eyeing his claims though. Kanye West appeared on the Timcast IRL podcast Kanye, or should I say “Ye, the artist formerly known as Kanye West”? Ye told Tim Pool: "I'm talking about literally finding out that they were trying to put me in prison this morning. But I found out — okay, so they froze, they put a $75 million hold on four of my accounts. And then they said, you owe a lot of taxes. Took me like six hours to find out how much. A lot — was it — well, around $50 million. “ I want to dissect these statements to share with you why I’m giving him the side-eye.

The Collections Process

When you owe a tax debt, there is a process the IRS follows to collect the debt. First, you’ll get a bill in the form of a CP14 Letter. Next, you’ll get a reminder, a CP501 letter. Then you’ll receive a reminder about the reminder, a CP503 letter. If you haven't responded to any of those letters, you'll receive a CP504 Letter - a Notice of Intent to Seize (Levy) your property. There are at least 4 letters that Kanye West should have received at his last known address. Notice of Intent to Levy Once the taxpayer doesn’t respond to those letters, then the notices of Intent to Levy are sent. As mentioned above, the first letter is the CP504 Notice of Intent to Levy. The Notice of Intent to Levy explains that the IRS intends to levy (seize funds) if the amount owed is not paid within 30 days. At some point, the taxpayer will receive the letter 1058. That's when the IRS has finally counted to three and decided to put their foot down and will levy your property. If you’ve been counting, from the time the tax is owed to the time the IRS even announces they are intending to levy your bank account can be upwards of 6 months. Please note that there is no mention of putting anyone in jail. By the IRSs' own processes, they didn’t ‘suddenly’ freeze $75,000,000. There has been ample opportunity to pay.

Ye said it took him 6 hours to find out how much he owes.

Sir, What? If Ye filed his taxes, he only needed to look at the tax return (s). I don’t care how you slice it, he had to have put his eyeballs on a tax return in order to sign it. We can only assume that he has a competent accountant. If that’s the case, it would have taken a phone call. He could have also logged into his IRS account. We’re going to just assume he doesn’t have an account, since many people do not. Him taking ‘6 hours to find out’ is ridiculous. Unless he was waiting for someone to get to work, it should not have taken him 6 hours to find out how much he owed in taxes. It may have taken him that long to find the letters and open them.

The IRS doesn’t resort to prison first

Now, back to Ye stating they were looking for him to put him in jail. While I was not there; I have a hard time believing this. I listened to the podcast, and he never specified exactly who was looking to put him in jail. He specifically said no one up to his house, but 'they' wanted to put him in jail. The IRS does not automatically put you in jail for owing taxes. If you owe, and you try to evade paying, then they will arrest you. Tax evasion is when you illegally don’t pay what you owe by hiding money, for example, or you try to flee the country without paying. That’s when the government puts you in jail. The only time the IRS will jump any of this process is if they believe they are dealing with someone who is a flight risk, or are concerned the taxpayer will try to dispose of assets to avoid paying taxes. Otherwise, they follow the process. My favorite part: After revealing he attempted to find out, “would this be tax evasion?” Kanye West then admitted, “I’m obviously not the most financially literate person on the planet.” Even the most financially illiterate person knows to pay taxes. #StopIt What’s the Take Away There is a collections process the IRS follows. It doesn’t go from you owing directly to levying wages and bank accounts. When you don’t respond to IRS letters, you force the IRS to enforce the law. Those laws are written by Congress, not the IRS. The IRS is the longest reaching arm of the law. If you have received letters from the IRS, open them, and then call us - 877.482.9411. We can help!

100% Bonus Depreciation Ends 12/31/22

Since we’re nearing the end of the year, business owners everywhere are looking for ways to save tax dollars. One of those ways is purchasing needed equipment or vehicles. If you NEED to replace equipment or a business vehicle, by all means, get it done before the end of 2022. Here’s why!

100% Bonus Depreciation is Ending

Since the Tax Cuts and Jobs Act of 2017, businesses have used bonus depreciation to deduct 100 percent of the cost of most types of property (other than real property). Starting January 1, 2023, bonus depreciation is scheduled to decline 20 percent each year until it reaches zero in 2027.

For example, if you purchase $150,000 in equipment for your business and place it in service [key detail] in 2022, you can deduct $150,000 using 100 percent bonus depreciation. If you wait until January 1, 2023, you’ll be able to deduct only $120,000 (80 percent). Don’t get me wrong, 80% bonus depreciation ain’t a bad deal. It’s just not 100%.

Cue the music for buying the G-Wagon! *insert smirk here* If there is any piece of influencer tax advice that irks my soul, it’s the ‘buy the G-Wagon’ advice.

It’s incomplete advice. Here’s how it works:

Let’s assume that on or before December 31, 2022, your business buys and places in service a new or used SUV or crossover vehicle that the manufacturer classifies as a truck, and has a gross vehicle weight rating (GVWR) of 6,001 pounds or more. This new, or new to you, purchased vehicle gives you four benefits:

- The ability to elect bonus depreciation of 100 percent

- The ability to select Section 179 expensing of up to $27,000

- MACRS depreciation using the five-year table

- No luxury limits on vehicle depreciation deductions

Example. On or before December 31, 2022, you buy your coveted G Wagon, a qualifying vehicle, and place it in service (use it for business purposes). The “cheap” G-Wagon SUV is $131,000, for which you can claim 100 percent business use. Your business cost is $131,000. Your maximum write-off for 2022 is $131,000.

And the crowd goes wiiiilllldddd!!!

Bonus Depreciation doesn’t mean free

When people hear this way cool tax advice, they make two unfortunate assumptions.

- The government is giving you a ‘free’ car.

- People also assume that the value of the car is a dollar-for-dollar reduction of the tax liability.

Neither of these is true.

You still gotta pay for the car.

No matter how you slice it, you must still pay for the car. It doesn’t matter if you pay cash for it, or if you have a loan. You may have been able to deduct the total cost on your tax return, which sounds sexy. You still have to settle up with whoever you’re purchasing the car from. The loan payments aren’t tax deductible either, only the interest paid on the loan.

Bonus Depreciation is not a tax credit

Story: I had a client call me and tell me she was going to buy a vehicle that qualified for bonus depreciation. The vehicle was $90,000. She assumed that her tax bill ($123,000) would be reduced by $90,000, consistent with being a tax credit. I explained that purchasing the vehicle would reduce her profit by $90,000, which reduced her taxable income. The purchase would reduce her tax bill by approximately $30,000.

If she had gone through with the purchase, she would have had to pay $90,000 for the vehicle, and still have to pay the remaining $93,000 tax bill ($183,000 out of pocket).

In the G-Wagon example, the vehicle would save you approximately $39,000 in taxes. You would end up paying $131,000 to save $39.000. That math ain’t mathin’ for me. You should purchase a vehicle or any business equipment, because when you need it, with the tax break being the bonus, not just to get a tax break.

Bonus Depreciation Fine Print

Since I know someone is going to be rushing out to buy a vehicle by the end of the year just to save on taxes, here’s the fine print you need to know.

-If you sell or trade the car before the end of its useful life (5 years), you have to pay tax on the depreciated amount (recapture), and it’s taxed as ordinary income.

-There is this teeny issue with the vehicle being an ordinary and necessary expense. Deductions are a matter of legislative grace. That means the government can disallow the deduction of an expense they deem is not ordinary or necessary.

-You can’t depreciate the vehicle AND take the standard mileage

-Vehicle must be used for at least 50% of business purpose

End-of-Year Tax Savings

By all means, do what you can to benefit your business and life, and as a result, lower your tax bill. That doesn’t mean you need to buy unnecessary things just because bonus depreciation is going away.

IRS Use of Private Collection Agencies

I received a frantic call from a new client. "HELP! I got a letter saying that the IRS referred my debt to a collection agency." The first question I had was why hadn’t they told me about the past tax debt. Actually, that was the only question I had, but anywho… While I totally get that collection agencies can be scary, I promise no collection agency is scarier than the IRS. If that’s the case, why does the IRS use outside collection agencies?

Use of Private Collection Agencies is Law

Congress passed a law requiring the IRS to use private collection agencies (PCAs) to help collect overdue taxes.

Your account is sent to a PCA if:

- The IRS was unable to locate you or didn’t have the resources available to locate you.

- A year has passed and you or your representative haven’t interacted with the IRS on your account.

- More than 2 years have passed since the assessment and the account was not assigned for collection.

Private Collection Agencies Used by the IRS

Effective September 23, 2021, when the IRS assigns your account to a private collection agency, one of these three agencies will contact you on the government's behalf:

CBE Group Inc. P.O. Box 2217, Waterloo, IA 50704 Phone: 800-910-5837

Coast Professional, Inc. P.O. Box 425, Geneseo, NY 14454 Phone: 888-928-0510

ConServe P.O. Box 307, Fairport, NY 14450 Phone: 844-853-4875

What's the process when your account is sent to a Private Collection Agency?

You will receive two letters before you are contacted by a private collection agency.

First, the IRS will send Notice CP40 and Publication 4518. As with any other letter you receive from the IRS, open the envelope and read the Notice CP40 carefully. It will tell you that your overdue account was assigned to a PCA. It will also contain important information on what you can expect to happen next.

Secondly, the private collection agency will send their initial contact letter. It has information on how to resolve your overdue taxes.

Both letters contain a Taxpayer Authentication Number. It’s used to confirm your identity. It’s also for you to verify that the caller is legitimate. Keep this number in a safe place.

Private Debt Collection Agencies Call

Unlike the IRS, PCAs will call you, but only AFTER they have sent their initial contact letter. Here’s what you should do when a PCA calls you.

- Validate that the caller is representing one of the private collection agencies listed above.

- The private collection agency will ask you a series of questions to verify that they’re talking to the right person.

- You will be asked for the Taxpayer Authentication Number with the private collection agency to validate each other’s identity.

- The private collection agency will be courteous, and professional and respect your taxpayer rights while following the laws.

- The private collection agency will work with you to resolve your overdue taxes. They will NOT threaten you. If you feel the private collection agency acted inappropriately, here’s how to report it.

How do you make payments to a Collection Agency?

YOU DON’T! Even though your account has been turned over to a PCA, you only make payments to the IRS.

You can use irs.gov/payments for electronic payment options. You can use IRS Direct Pay to use direct debit (from your checking or savings account), preauthorized Direct Debit, the Electronic Federal Tax Payment System (EFTPS), or you can pay by check/money order payable to the United States Treasury.

If you use a check or money order, write your name, Social Security number, and tax year on your payment. The private collection agency will provide the appropriate IRS mailing address for the payment, or you can find it here. Even though you can mail a payment to the IRS, only use it as a last resort. Paying online is faster and more secure.

Private Collection Agencies have no enforcement authority

Private collection agencies cannot take any type of enforcement action against you to collect your debt. However, the IRS does have the legal authority to file a Notice of Federal Tax Lien (against any property) or issue a levy (take money from your bank account) to collect an overdue account.

Don’t want to deal with the PCA?

If you don’t want to deal with the collection agency, you can have your account moved back to the IRS. You must submit this request in writing to the PCA.

Takeaways -

Having your account sent to a PCA isn’t the worst thing in the world. It just means that the IRS couldn’t find you. The IRS will mail letters to your last known address. If you’ve moved and haven't filed past due returns, the IRS may not have a good address for you. They aren’t gonna hunt you down. They will simply turn your account over to a PCA.

If you have unfiled returns or unresolved tax debt, reach out to us at ETS Tax Relief: 877.482.9411.

1099K Change for 2023

The IRS issued a press release on October 24, 2022 reminding service providers and other business owners that they may receive a form 1099-K for sales in excess of $600. Third-party payment processors such as PayPal and Stripe will issue 1099-Ks to their customers in early 2023 for sales that exceed $600, regardless of the number of transactions. This will impact tax returns filed in 2023 for Tax Year 2022.

Prior to 2022, third-party payment processors issued form 1099-K if the total number of transactions exceeded 200 AND the total amount of the transactions exceeded $20,000 for businesses. Here are some examples.

Scenario 1: A provider had 3 transactions totaling $25,000. A 1099-K was not issued, because the number of transactions did not exceed 200.

Scenario 2: A provider had 1000 transactions, but the total sales amount was $19,000. A 1099-K was not issued, because even though the number of transactions exceeded 200, the amount of sales was less than $20,000.

![]()

As taxpayers became aware of the reporting requirements, many did not report the income on their taxes. There were also taxpayers that used more than one third party processor in order to avoid reporting requirements. This act is called structuring, and it’s illegal.

The American Rescue Plan Act of 2021 (ARPA) lowered the reporting threshold for third-party networks that process payments for those doing business. Now a single transaction exceeding $600 can trigger a 1099-K. But, why?

Who is TIGTA?

While the media will have you believe that all of this happened because of a President and his administration, this change in reporting was coming regardless of who was in office. Here’s why:

On December 30, 2020, The Treasury Inspector General for Tax Administration (TIGTA) released a report: Billions in Potential Taxes Went Unaddressed From Unfiled Returns and Underreported Income by Taxpayers That Received Form 1099-K Income. TIGTA is an independent organization that provides oversight of the IRS.

TIGTA reviewed 2017 tax returns to compile their report. The report states, “TIGTA identified 314,586 business taxpayers with $335.5 billion in Form 1099-K income that appeared to have a filing obligation, but were not identified as nonfilers by the IRS.” …”TIGTA identified a significant number (325,060 business non-filers and 103,991 individual non-filers with $203 billion and $3 billion in Form 1099-K income, respectively) that were not selected to be worked.”

Essentially TIGTA revealed the abuse of 1099-K reporting requirements and recommended the IRS fix it. That’s why the law changed. It had nothing to do with the President.

What about the Zelle “Loophole”?

After ARPA 2021 was released, there were several social media posts created about the ‘Zelle Loophole’. Zelle is a money transfer application that allows you to transfer money directly from one bank to another. It is not a third-party payment processor. Because of that, Zelle currently has no reporting requirements.

Social media influencers were suggesting that using the “Zelle Loophole” was a legal way to circumvent the 1099-K reporting requirements. This is absolutely and unequivocally FALSE.

Using Zelle to earn income and not report it is tax evasion - the illegal non-payment or under-payment of taxes, such as by declaring less income, profits or gains than the amounts actually earned, or by overstating deductions. Zelle’s terms of service also states: “We only grant you a limited revocable license to use the Site for your own non-commercial use subject to rules and limitations.” In other words, you’re not supposed to use it to receive business payments.

Reputable sites were purporting the myth that the IRS was going to “start” taxing money that wasn’t previously taxable. That is inherently false. Do not confuse ‘third party reporting requirements’ with your responsibility to report your income. Section 61(a) of the Internal Revenue Code defines gross income as income from whatever source derived, including (but not limited to) “compensation for services, including fees, commissions, fringe benefits, and similar items.” I.R.C. § 61(a)(1). All income is taxable unless there is a specific provision that says it’s not. You’re even required to report stolen money!

Prior to 2022, you were required to report your income, even though third party processors were not required to issue 1099-Ks. The requirement for the taxpayer to report their income is not new. The change in third party reporting requirements is what’s new.

States were already making the change

There were a few states that already lowered the threshold for reporting. Maryland, Massachusetts, Virginia, Vermont, and District of Columbia had already reduced their reporting requirement to $600 in previous years. There are other states that had lower reporting requirements, as well. Now it will be reported uniformly in all states.

If you have previously avoided reporting your income, we highly encourage you to amend those returns to accurately reflect what you earned. Give us a call if you need help: 877.482.9411.