Can Service Providers Issue a 1099-C for Unpaid Bills?

Social media never fails to provide the most false or misleading tax information. This post did not disappoint. The social media post said:

$130K in unpaid contracts over here.

I don’t argue. I have forgiven their debt on my end with a 1099-C.

Now it’s between them and the IRS beloveds. It’s above me now.

If you do B2B transactions do not argue. Make their debt to you taxable. They do not get to claim a tax break when they did not start or finish paying you.

Protect your business and your blood pressure 😊

The post was made by a service provider who had unpaid bills. The post had 20 comments and 597 likes. Almost 600 people saw this post, and thought ‘this is really cool’. A few others commented that ‘this was an education’, and others stated that they were going to do this ASAP! Uhhh NO!!

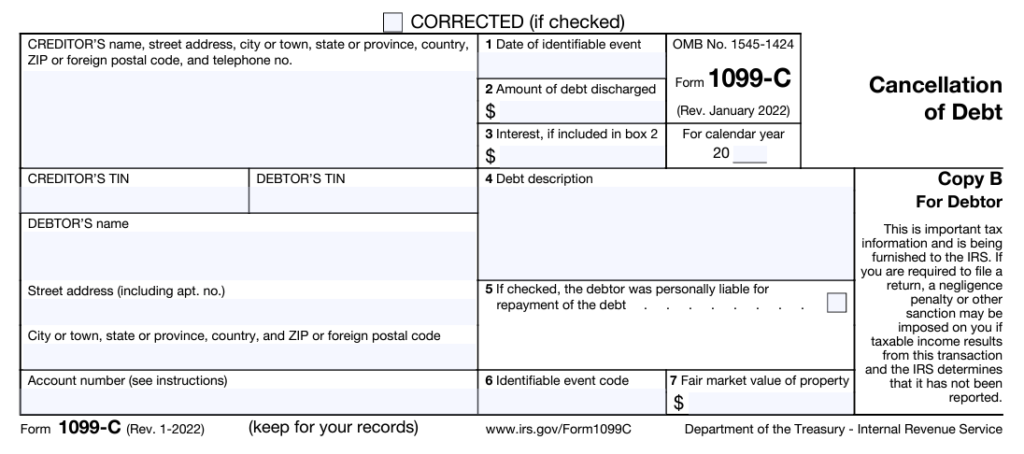

Purpose of a 1099-C Cancellation of Debt

The IRS form 1099-C, Cancellation of Debt, is designed for financial institutions (such as banks) to report a cancellation of debt [usually related to non-payment] of $600 or more. This cancellation of debt, most often, is treated as taxable income to the debtor, and must be claimed on the tax return. A creditor/debtor relationship is established. There is a loan amount, loan payment terms, interest rate, and methods of resolution in the event of default (non-payment).

Who Can File a 1099-C

Internal Revenue Code 6050P makes a specific list of entities who can file a 1099-C:

- A financial institution described in section 581 or 591(a) (such as a domestic bank, trust company, building and loan association, or savings and loan association).

- A credit union.

- Any of the following, its successor, or subunit of one of the following.

- Federal Deposit Insurance Corporation.

- National Credit Union Administration.

- Any other federal executive agency, including government corporations.

- Any military department.

- U.S. Postal Service.

- Postal Rate Commission.

- A corporation that is a subsidiary of a financial institution or credit union, but only if, because of your affiliation, you are subject to supervision and examination by a federal or state regulatory agency.

- A federal government agency including:

- A department,

- An agency,

- A court or court administrative office, or

- An instrumentality in the judicial or legislative branch of the government.

- Any organization whose significant trade or business is the lending of money, such as a finance company or credit card company (whether or not affiliated with a financial institution). The lending of money is a significant trade or business if money is lent on a regular and continuing basis.

Please note that you do not see a service provider with an unpaid bill in the list.

Providing a Service does not create a Creditor/Debtor Relationship

When a service provider engages a client for services, It creates a provider/client relationship. A service provider agrees to perform a service in exchange for an agreed amount. There are remittance (payment terms), such as payment due in 15 days, due immediately upon completion, or due in advance. While this is a contract, it does not create a creditor/debtor relationship. The service provider is not lending money to the client.

Filing a False 1099-C Consequences

This service provider seemed really snappy and clappy, seemingly to believe that she will cause their client to have an unexpected tax bill. However, should she issue a 1099-C for an unpaid bill, there are consequences.

Internal Revenue Code 7434 states:

If any person willfully files a fraudulent information return with respect to payments purported to be made to any other person, such other person may bring a civil action for damages against the person so filing such return.

https://www.law.cornell.edu/uscode/text/26/7434

The person filing the false 1099-C can be liable for the GREATER of $5,000 or the sum of damages, costs of the action, and attorney’s fees. A plaintiff (the one who received said 1099-C) has 6 years from the date the false 1099-C was filed or 1 year after the return would have been discovered with reasonable care. Oh yeah, the IRS wants a copy of the suit, as well.

It can be quite frustrating when you provide a service to your client, and they don’t pay the bill. You can go through a collection agency to try to recoup your money. You cannot deduct the amount of unpaid funds, unless you’re using the accrual method of accounting. The only reason it is a deduction for the accrual method is that you’ve already counted the income. Regardless, issuing a 1099-C is not the method for service providers to collect their unpaid funds.

If you are dealing with back taxes or unpaid tax debt, reach out to us! We’re here to help!

More Related Articles

BEWARE Military Disability Scam

My husband retired from the military in April 2022. It was an awesome occasion when it finally got here; however, getting there was slightly painful. He had to go through tons of briefings on his…

1099K Reporting 2024

There has been another delay in the change of the 1099K reporting. It has also caused more confusion for payors to know if they should issue a 1099K or a 1099-NEC to a provider. Let’s chat about how…

Employee Gifts are Taxable

I was perusing the news a few weeks ago. The news headlines said, “Wal-Mart Slammed After Gifting Employees 55-Cent Ramen Noodles” for working during a blizzard. Needless to say, Wal-Mart was…